0 Divorce and Social Security: Your Ex's Record Might Still Pay Off

- Divorce

- by William F. Davis, CFP®

- 03/06/2025

Divorce is a financial gut punch—splitting assets, rewriting budgets, maybe even selling the house you swore you’d never leave. But here’s a twist you might not see coming: your ex’s Social Security could still have your back. Yep, even after the ink’s dry, there’s a chance to claim benefits based on their record. Don’t get too excited—it’s not a jackpot, but it’s a lever worth pulling if the numbers line up.

First, the ground rules. You can tap into your ex’s Social Security if the marriage lasted at least 10 years, you’re 62 or older, and you haven’t remarried. (Remarriage is the kill switch here—tie the knot again, and this option’s toast.) Oh, and your ex? They need to be eligible for benefits too, though they don’t have to be collecting yet. The kicker: your own benefit has to be smaller than what you’d get off their record. If it’s not, you’re stuck with yours. Fair? Maybe not. Practical? Absolutely.

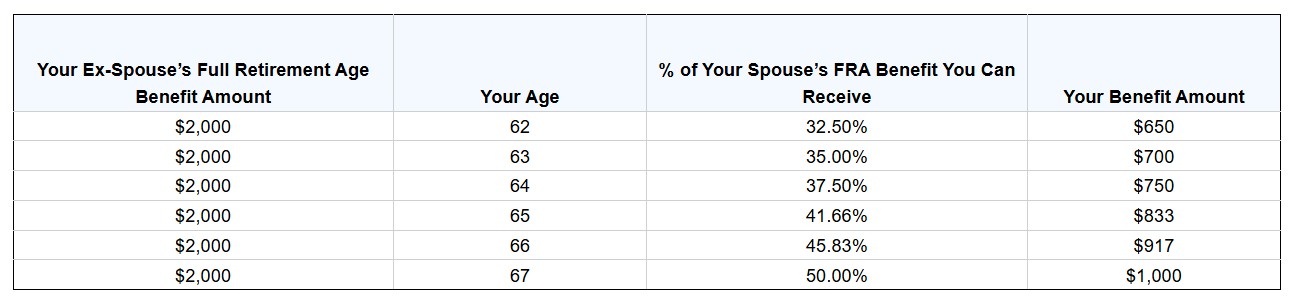

Now, let’s talk timing, because this is where it gets interesting. Claiming early—at 62—shrinks your payout, while waiting until your full retirement age (somewhere between 66 and 67, depending on when you were born) keeps it intact. Delay past that, and it grows a bit until 70.

Figure 1 below lays it out clean: early birds get less, patient types get more. It’s a choice that can swing your monthly check by hundreds.

Here’s the rub: you don’t need your ex’s blessing. No awkward phone call, no sign-off required. The Social Security Administration doesn’t even tip them off—it’s all between you and the feds. That said, don’t expect them to spoon-feed you the details. You’ll need your marriage and divorce docs handy, and probably a few hours to wrestle with the paperwork. Pro tip: call ahead or hit SSA.gov unless you fancy a day trip to the local office.

What’s the payoff? Up to 50% of your ex’s benefit at their full retirement age, assuming it beats your own. If they’re a high earner and you’re not, that’s real money—maybe enough to offset the hit from splitting the 401(k). But it’s not extra cash on top of your own benefit; it’s an either/or deal. The system compares the two and hands you the bigger slice. Simple, not generous.

Divorce might’ve torched the “happily ever after,” but it doesn’t have to torch your retirement. This benefit’s a quiet perk—easy to miss if you’re not paying attention. So, dig out those old records, run the numbers, and see if your ex’s work history can still do you a solid. It’s not revenge – it’s just good financial sense.

0 Comments

- There is no comment found.