0 Vericrest Insights - April 2025

- Vericrest Insights

- by William F. Davis, CFP®

- 04/03/2025

We are going to start off with some perspective….

“I need to get out now and wait until the market comes back.”

"I'll wait until the market pulls back before I add more."

These are examples of investors who do not have an overall plan. When investors talk like this – and, worse yet, make investment decisions like the – it’s clear that they do not have an overall plan. In fact, their “plan” changes with each passing market gyration.

much does the market need to come back?” or “How much does the market need to drop?” 5%? 10%? 20%? 35%? More?!?!

Why Financial Planning Matters Now

Well, we know that, on average, we're going to see a

- 5% correction about twice a year

- 10% correction about every 18 to 24 months

- 15% correction about every three years

- 20% or more about every six years

So what do we do about it? Well, we should be investing according to what we need our assets to do. Your investment timeframe and your own personal ability to tolerate risk will ultimately drive the conversation and the investment decision.

Think about it. There's a big difference between a retiree who needs those funds for current income and a 25-year-old who has 40+ years to let compounding growth do its thing. But what about a 30-year-old who wants to buy a house this year and has $150k saved? What about a family of 5 who is changing careers and wants to take some time off before they jump into their next adventure? What about the 45-year-old who is saving aggressively to retire in 10 years? Or the 67-year-old who is retiring at the end of the year and will begin taking monthly distributions.

These investors cannot all allocate the same way. And this is where financial planning helps to figure this out – while taking into account the ups and downs of market cycles. What can derail a plan, however, is letting the emotional weight of anxiety and fear dictate investment decisions.

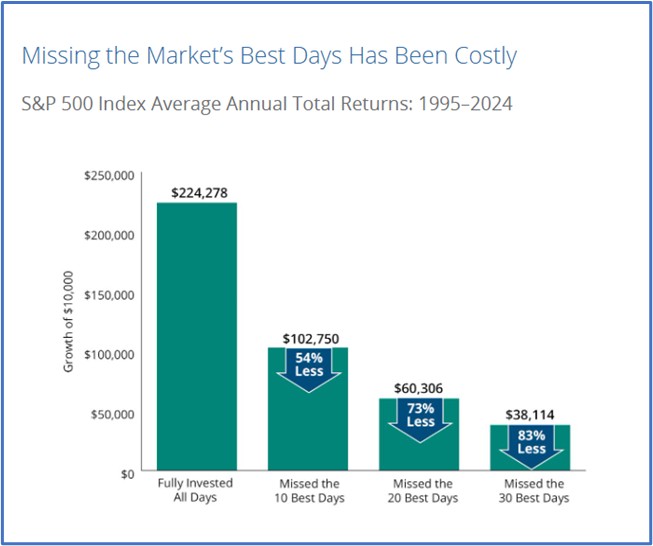

Missing the Best Days Costs You Big

Avoiding the market’s downs may mean missing out on the ups as well. Seventy-eight percent of the stock market’s best days have occurred during a bear market or during the first two months of a bull market.

Here’s something more to consider: If you missed just the 10 best trading days in the S&P 500 over the past 20 years, your total returns would be cut in half. And missing the best 30 days would have reduced your returns by 83%!

The kicker? Many of those best days occur in the depths of a market downturn, when most people are too scared to invest.

Market Commentary

The first quarter of 2025 saw rising trade tensions and geopolitical uncertainty upset markets. While both the U.S. labor market and U.S. consumer spending remain solid, a deterioration in growth expectations has emerged at the same time as inflation expectations have risen.

From a monetary policy standpoint, the Federal Reserve continues to signal a “data dependent” path, but the likelihood of aggressive easing has diminished. Elevated inflation expectations, driven largely by proposed tariffs, have pushed the “Fed put” further out of reach. The Fed is unlikely to act preemptively unless there is clear evidence of labor market weakness or a sharp tightening in financial conditions. Market pricing, which once anticipated up to five rate cuts in 2025 (!) has recalibrated to reflect a more cautious stance.

In response, markets have moved aggressively to reprice these risks, with U S equities and the dollar undergoing a sharp sell-off. After posting new highs in February, the S&P 500 Index fell by 10 through the end of the quarter. As of the writing of this note, the uncertainty around the tariff issue is still driving market gyrations – the market does not like uncertainty.

Another reason for stock market fragility is that valuations are no longer cheap. The S&P 500 Price-to-Earnings (P/E) ratio, for instance, is 20.2 times next-12-month earnings, which is above the long-term average. In this environment, diversification across various market segments, including value stocks, international equities, and fixed income, can help manage risk while positioning portfolios for long-term growth.

Portfolios

We rebalanced our portfolios this week, so you should be receiving those trade confirmation notifications.

Our portfolios continue to remain modestly tilted to U.S. stocks relative to bonds and continue to favor companies with attractive yield and profitability metrics. While valuations on market cap-weighted indexes remain elevated compared to history, the broader market (mid/small caps) remain priced at a meaningful discount to large growth stocks. European equities have seen a tailwind from a surprising, post-election fiscal pivot in Germany. The passage of an infrastructure and defense bill represents a meaningful shift in policy and as a result, GDP forecasts for the Euro area increased markedly.

In U.S. fixed income, Treasury yields have generally been a good hedge for risk assets over the course of the quarter. In credit markets, spreads have widened modestly, as volatility in equity markets has negatively impacted sentiment. The sharp rise in economic policy uncertainty suggests that further tightening in credit conditions could emerge if recession fears intensify. Uncertainty, moderate economic growth, and slower than expected disinflation have kept the Fed in check so far, but mounting growth concerns have raised expectations for more rate cuts later this year. We continue to have our largest fixed income holdings in U.S. bonds (AGG) and mortgage-backed securities – two allocations that have driven our performance vs. equities.

Going forward, we will continue to keep an eye on the Fed, and make adjustments accordingly.

Lastly, and most importantly, we should point out that in spite of all the headlines and volatility over the past few weeks, little damage has been done to diversified portfolios. Yes, you can log in and take a look :)

Sure, portfolio allocations concentrated in aggressive growth have taken a big hit. That’s to be expected. But looking at Morningstar benchmarks for balanced portfolios across the risk spectrum, thanks to the strong returns of core bonds, international equities, and dividend-paying equities, the year-to-date performance of most well diversified portfolios is still close to flat for the year. In other words – nothing to get excited about.

So, while the current situation certainly bears monitoring, and we will, we should all try hard not to overreact prematurely to what is really just normal volatility, albeit triggered by some abnormal developments.

As always, I am available to answer any questions you may have. And as always, I appreciate your trust in me.

Hope you and your family enjoy the spring!

Additional Reading

Here are some articles that I have found both interesting and relevant.

3 Reasons to Stay Invested Right Now

10 Habits of Financially Successful People

12 States with the Lowest Property Taxes: 2025

Is Domino’s pizza inflation-proof?

0 Comments

- There is no comment found.