Mutual fund fees can be sky high - know when you’re overpaying!

There is talk of the fees associated with investing in mutual funds, but much less clarity on the question of how high is too high a mutual fund fee. In this blog we’re going to discuss what mutual fund fees are composed of, what the average mutual fund fees are, and what is too high.

What is a mutual fund fee?

When you buy, or subscribe into, a mutual fund, fees are automatically deducted from the amount you directed towards the fund. You don’t pay directly by writing a check or sending the money in.

These fees are used to compensate the mutual fund company, and they fall into these major categories:

- Operational – managing the fund’s assets, researching what securities to buy and sell, etc.

- Administrative – legal, accounting, and custodial expenses

- Marketing – this covers compensations to the person who sells the fund to new shareholders, the cost of marketing materials, and other forms of distribution.

You can find out how much in fees the fund is charging by looking at the prospectus. A prospectus is a document that must be given to each shareholder who subscribes to the fund. It outlines the fund’s objectives, investment characteristics, expenses, and other legal and operational information. It also states the names of the individuals responsible for making investment decisions for the fund, called the fund or portfolio managers.

The mutual fund fees are calculated against the total amount of assets in the fee to yield the mutual fund expense ratio. Now, this is not to say that is all you’ll pay. Depending on how you buy into the fund, you may be responsible for paying transaction fees, commissions, or other fees charged by the brokerage firm or custodian involved.

How to find out what a mutual fund’s fees are

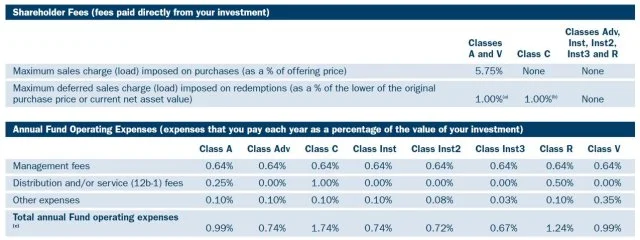

The prospects contains quite a bit of information, and for that reason many prospectuses are available in summary as well as full form. Take for example the Columbia Large Cap Growth Fund. The prospectus displays the following fee information:

The fund hasn’t broken out the fees in great detail, but you can see the expense ratios broken out on the bottom line of the chart. Let’s look at how this works out for potential investors.

Suppose that:

- You bought the Class C shares of this fund, with a 1.74% expense ratio.

- You were to invest $100,000 in that fund.

- You pay $1,740.00 to the fund in mutual fund fees which are used to compensate the fund for its expenses incurred over the span of a year.

Quite a chunk of change to be paying, no?

When am I paying too much?

Fidelity cites the average mutual fund fee for equity funds to be 1.4%. We think this is too high. In fact, we feel that more than 1% fees is too high.

Think about the impact that fees have on investment returns. A percentage point may not seem like a big deal, but it is. We’ve discussed this in depth, with specific examples of how much you are losing by paying high fees for your investments, in other blogs:

Why 12b-1 fees take a big bite of your portfolio!

Average financial advisor fees – are you paying more than you should be?

What do Financial Advisors Cost?

If you are investing under the guidance of a financial advisor, you also would need to take into account the impact of that advisor’s fees. If you are paying that additional layer of fees, the total amount can be very significant.

Take this example:

- You own a $1MM portfolio of funds with an average 1.4% expense ratio (the average mutual fund fee). One of the main drivers of expense is the 12b-1 fee that the mutual fund charges to compensate the fund for the marketing of the fund.

- Your financial advisor charges 1% on top of that.

- You are shelling out 2.4% of your portfolio value, or $2,400, to the mutual fund family and the financial advisor in fees alone!

On top of that, you may have to pay transaction costs paid to the custodian or broker.

Why we avoid mutual funds altogether

As wealth managers, we see the impact of fee layering, high 12b-1 fees, and high mutual fund fees in portfolios that people bring to us for review. We prefer to invest in low cost ETFs instead which have a very clear cost advantage over mutual funds. Aside from having lower expense ratios and an absence of 12b-1 fees, they offer flexibility, diversification, and tax efficiency.

We are a fiduciary financial advisor in the Philadelphia area, but we work with clients across the country. We provide fee-only, objective advice to our clients. If you would like to discuss a possible relationship, contact us.

Sources

Fidelity Investments. ETFs vs. mutual funds: Cost comparison. Retrieved in Jan 2022 from here

Columbia Threadneedle Investments. (December 1, 2021) Columbia Large Cap Growth Fund Prospectus. Retrieved from February 8th, 2022 from here