Interval Funds: what to know before you invest

One of the newest investment vehicles on the scene is interval funds. We’ve found other discussions of interval funds to be quite uninformative. In this blog we’ll discuss what they are, what their inner workings typically look like, and when it does and does not make sense for an investor.

Before we get started, you may want to take a moment to read our other blogs on mutual fund investing.

A share mutual funds – run away!

First - understand open vs. closed end funds

Here’s where we feel others mess up the definition of interval fund: You have to understand the difference between an open and closed end mutual fund before you can grasp what an interval fund is.

There are two major types of pooled investment vehicles that are gaining some visibility with investors.

An open-end mutual fund:

- Does not trade on an exchange.

- Has an unlimited number of shares.

- When you buy into an open-end mutual fund, new shares are created using the funds you deposited. On the converse, when you redeem, the fund buys your shares back using cash from the fund, or it may have to sell some of its holdings to create liquidity.

- You can effectuate a transaction any time you wish, but it is only executed at the closing day price and the shares don’t move until after the fund closes for the day.

- Is regulated under the Investment Company Act of 1940 and must file reports with the Securities and Exchange Commission

- Are bought and sold at the Net Asset Value, or NAV

A closed-end mutual fund:

- Usually trades on an exchange.

- Has a limited number of shares.

- When you buy into a closed-end fund, no new shares are created. You are simply picking up shares that another investor is offering to sell.

- You can trade intraday.

- Is regulated under the Investment Company Act of 1940 and must file reports with the Securities and Exchange Commission

- Is bought and sold by the price determined by supply and demand for the fund

These definitions are important to know if you are considering investing in any type of mutual fund. Don’t just trust whatever your broker or advisor says. Do your own research and know what you are owning, just to be safe.

What is an interval fund?

An interval fund is defined as a closed end fund that does not trade on an exchange that offers periodic liquidity.

Wow! That was a mouthful.

Here’s how interval funds are different from the typical closed-end fund (U.S Securities and Exchange Commission, ND).

- Unlike most closed-end funds, they do not trade on an exchange

- The fund itself will buy or sell shares directly from or to the consumer instead of these transactions happening through the exchange.

- You may be able to purchase shares at any point.

- You are only able to sell shares back to the fund at a specific time, which the fund specifies in its prospectus.

- Bought and sold at a priced based on the NAV, that is not known at the time the repurchase offer is made.

- You aren’t able to redeem your entire investment amount at once.

- There may be a 2% redemption fee.

- There may be higher management fees.

Interval fund vs. mutual fund

Aside from the differences mentioned above, interval funds often pursue a different investment strategy that most mutual funds. They can use leverage, and many times they run what many investors consider alternative asset strategies such as real estate debt, credit, or direct lending. These strategies tend to offer higher yield but offer less liquidity.

History of interval funds

Interval funds have an interesting history (Interval Funds, ND). They have been around since the 1990s, but with the recent popularity of exchange traded funds, they became less notable. After the 2008 recession, closed end funds started to become more popular and interest in interval funds rose along with them. Decreased regulation made it easier for fund vehicles to invest in alternative asset classes such as private equity.

Who it makes sense for

The investment objective of every fund is different, and a person’s strategy is dependent upon a number of different factors. On balance, interval funds are usually chosen by people who:

- Is looking to invest in less liquid instruments

- Desires yield

- Wants a return that is non-correlated with the market

- Don’t have high liquidity needs, as many interval funds have gated redemptions, prohibiting the investor from having free access to the money held in the fund.

- Do not require the ability to liquidate their investments immediately; has additional funds saved for a crisis

- Has done enough financial planning to feel confident in their gauge of future expenses and cash flows

- Is not highly fee conscious

Who it doesn’t make sense for

Intervals funds are not a wise choice for someone who:

- Requires immediate or short-term liquidity

- Does not have funds saved to support living expenses outside of the money invested in the fund

- Doesn’t have a financial plan or a clear concept of future cash flows

- Is highly fee conscious

- Need certainty about short term access to their funds

What to ask yourself before buying an interval fund

If you are thinking of investing in an interval fund, here are some questions to ask yourself before you do so.

- Could I survive without this money, if I had a sudden need for cash? If so, for how long?

One of the benefits of working with a financial advisor is the ability to gain clarity about cash flows. Many financial advisors will help clients by creating a financial plan that maps out their expenses and the cash flows projected to cover them. This may give you a sense of how much excess cash is given at any one point, and how much you can invest in the market. Along with an overall assessment of your risks and life goals, an understanding of your liquidity needs may be reached.

All of this should be outlined in the Investment Policy Statement that an advisor puts together for you in the beginning of a relationship, and revisits through the duration.

- What are the fees?

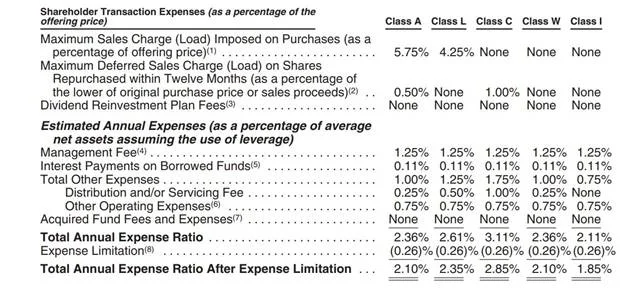

The fees for any mutual fund are disclosed in the fund’s prospectus that is required to be delivered at the time of purchase by the 1933 Act. It is imperative that you understand any and all interval fund fees before putting your money into these vehicles.

Take, for example, the Goldman Sachs Real Estate Diversified Income Fund (GSREX) prospectus (Goldman Sachs Asset Management, 2022). It is useful to search on the term “Fee Table” within the prospectus. Most have a section called “fund fees and expenses” or the like which outlines all the fees you could potentially pay by investing in the fund.

Know what each type of fee is. In the above fee schedule, here’s how these fees would be defined.

- Sales Load – a commission paid to the broker who sold you the fund.

- Redemption fee – if you redeem the shares within a certain period, you are due to pay a fee.

- Management fees – fees paid to the portfolio manager for managing the fund

- Interest payments on borrowed funds – if the fund is using leverage, you’ll likely be paying interest on the line of credit they took out to borrow the funds

- Operating expenses – legal, accounting, custodial expenses

- Distribution fee – fee you pay to compensate the fund for marketing itself

As you can see, there are quite a few fees to be aware of. It’s imperative that investors can gain an understanding of the fees; do not invest without doing the research.

- What are the liquidity constraints I would be facing if I were to put my money into this fund?

Repurchase terms vary by fund. To quote the Goldman Sachs fund prospectus mentioned above:

The Fund operates as an “interval fund” (defined below) pursuant to which it will, subject to applicable law, conduct quarterly repurchase offers for between 5% and 25% of the Fund’s outstanding Shares at net asset value (“NAV”).

And in another place:

An investment in the Fund is not suitable for investors who need certainty about their ability to access all of the money they invest in the short term. Even though the Fund will make quarterly repurchase offers for its outstanding Shares (expected to be 5% per quarter), investors should consider Shares of the Fund to be an illiquid investment. In addition, there is no active secondary market for Shares. There is no guarantee that investors will be able to sell their Shares at any given time or in the quantity that they desire

Every interval fund has different terms; this is merely an example. However, we do take the view that given the uncertainty of redemption, you should consider any investment in an interval fund to be an illiquid investment. Even though they are somewhat illiquid, there is more liquidity compared to private funds or alternative assets.

Final thoughts on interval funds

Investing in an interval fund isn’t something to be taken lightly. There are liquidity constraints and the fees can be burdensome.

Before doing so, we recommend that you conduct thorough diligence and proceed with caution. It’s important to find the right interval fund for you, if you chose to go this way. Many times, a financial advisors can be of assistance in determining your liquidity needs, the suitability of such investments, and your overall cash flow budget.

We are a fiduciary financial advisor in the Philadelphia area, but we work with clients across the country. We provide fee-only, objective advice to our clients. If you would like to discuss a possible relationship, contact us.

Sources

Goldman Sachs Asset Management. Goldman Sachs Real Estate Diversified Income Fund. Retrieved from here.

Goldman Sachs Asset Management. Goldman Sachs Real Estate Diversified Income Fund.(28 January, 2022). Prospectus. Retrieved from here.

Interval Funds. (Sept 09, 10:53). The History of Interval Funds – and Where They’re Heading. Retrieved from here.

Investor.gov. ND. U.S Securities and Exchange Commission. Interval Fund. Retrieved from here.

U.S Securities and Exchange Commission. (2020, Sept 25th). Investor Alerts and Bulletins. Investor Bulletin: Interval Funds. Retrieved from here.