Say “no” to A share mutual funds!

Despite the availability of lower cost options, investors continue to buy A share mutual funds. They shouldn’t. In this blog we’ll talk about why we think investors should run away as fast as they can from A share mutual funds, and we’ll refute the fake logic of the hollow sales pitches that people are often given to urge them to invest in these vehicles.

Get ready for an eye-opening analysis!

But first, we are low fee financial advisors in Philadelphia, PA. We feel passionate about low-cost investing, and wrote these blogs you may want to check out:

Mutual fund fees can be sky high

12b-1 fees take a big bite out of your portfolio

Financial advisor fees – are you overpaying?

How investors lose money

Before we get started on our crusade against A share mutual funds, let’s take a moment to discuss how investors lose money.

So, you have a portfolio. Sometimes it goes up, and sometimes it goes down. It’s all the market’s fault, right?

Well, not exactly. There are two very large factors that play a part in your portfolio performance.

#1 Cost of investment erodes returns

Your portfolio may be riddled with higher fees than necessary. True, if you need a financial advisor, that costs money. Buying pooled vehicles such as ETFs or mutual funds costs money. But with so many options available, there’s no reason you should be getting price gauged, which is unfortunately the case when people buy A share mutual funds.

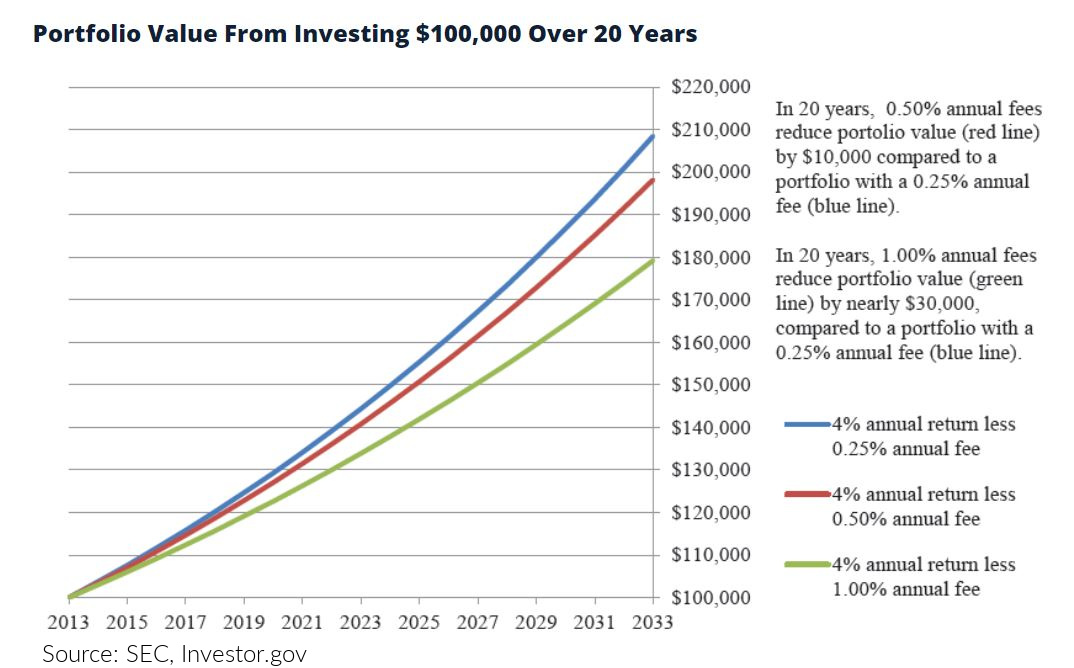

You may not even consciously be aware of it, but your portfolio, over time, may be suffering from the effects of a mutual fund management fee that is taking more than it should out of your portfolio. Compounded over time, this can have a big effect.

Look at what the impact of mutual fund fees can be on your wealth - this graph from Investor.gov just says it all:

There’s nothing wrong with using mutual funds, ETFs, or with hiring a financial advisor. But if you choose to go that route, you should always make sure that the fee you’re paying comes with commensurate value to the benefit provided.

It’s not always easy – sometimes the terms aren’t clear – and we’ll get to that in a little bit.

#2 Biases derail investor performance

Most investors, if left to their own devices, will wind up not beating the market, or in many cases, not even performing in line with it, as confirmed by numerous Dalbar studies.

Our blog about investor bias covers the eight psychological traps that investors tend to fall into. In alphabetical order, they are:

- Action bias

- Anchoring bias

- Confirmation bias

- Disposition bias

- Familiarity bias

- Loss Aversion

- Self-aversion bias

- Trend-chasing bias

These psychological biases are deeply engrained in each investor’s mind, and one of the best ways to overcome it is to work with a financial advisor who can provide behavioral coaching to help you stay grounded and avoid the pitfalls.

There are many subtopics within both categories, but for now let’s just focus on one of them: A share mutual funds and how they are a rotten option for investors who want to accumulate long term wealth.

What is an A share mutual fund?

An A share mutual fund is defined as a mutual fund that charges a sales load for you to invest in it. In addition, the mutual fund has an ongoing expense ratio that is paid out of the invested amount, which may include a 12b-1 fee.

Whoa whoa, we threw some terms at you. Let’s slow down and define them.

A sales load is a commission paid to the broker who sold you the fund. In an A shares mutual fund, the sales load can be as high as 5.75%. So, if you were to invest $100,000 in the fund, the broker who sold you the fund would pocket $5,750.

Quite a big bite, no?

With so many low-cost ETFs and no-load mutual funds available (both of which charge zero sales load whatsoever), we feel there is no need for anyone to pay a sales load anymore.

What is a mutual fund expense ratio?

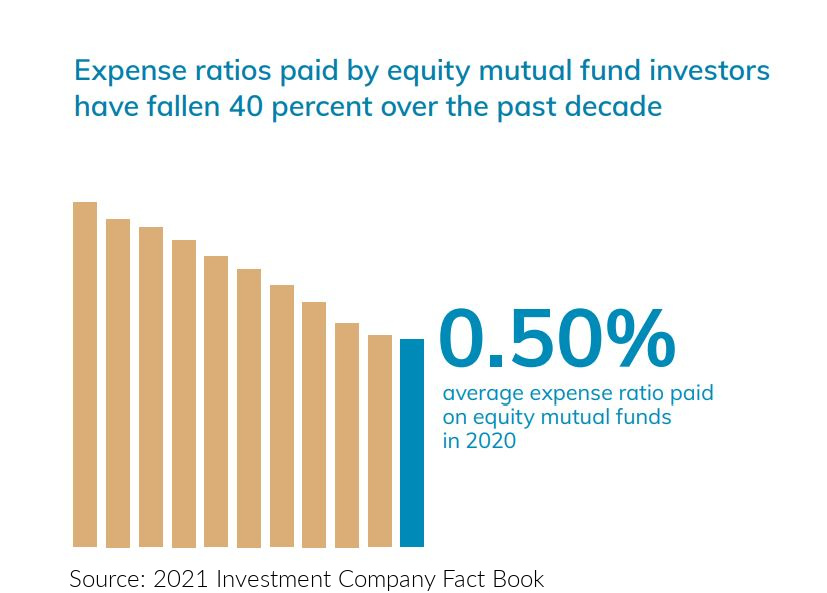

The expense ratio is paid directly to the mutual fund company. It compensates the fund management company for administering, marketing, and managing the assets in the fund. The average equity mutual fund expense ratio is 0.50% (Investment Company Institute, 2021) and just to reiterate, this is paid out of the portfolio in addition to any sales loads

What is a 12b-1 fee?

A 12b-1 fee is paid to the mutual fund company. It is included in the overall expense ratio. Essentially, it pays the fund for the sales and marketing related expenses incurred for selling the fund to you. By law it can’t be greater than 1%.

Enough fees for ya?

By the way, some mutual funds offer breakpoints, a scenario in which you receive a discount off the sales load for purchasing a certain amount of the fund. Mutual fund breakpoints are disclosed in the fund’s prospectus. Breakpoint discounts may be recognized for a lump sum investment, or a series of investments over time. However, in the latter case, you must sign a letter of intent stating the dollar amount that you are committing to invest in the fund.

Confused yet?

If you’re like most people, you are! It’s important to understand how mutual fund fees work though, before you invest.

What is a mutual fund share class, and why do they exist?

You can just imagine how in days of yore, with all these different fee structures abounding, things became a bit overwhelming for investors. To clarify matters, the SEC came up with what are called mutual fund share classes. There are four: A, B, C, and D. Here is a great explanation of each of the mutual fund share classes. This was done under Rule 18F-3, passed in 1995.

As Class A shares is the subject of our article, we’ll just focus on that for now. Class A mutual funds:

- Have a front-end sales load which is debited out when you buy it

- Have a lower 12b-1 fee than the other classes

- Are usually sold directly to investors by brokers

- Debit out ongoing expenses for the administration and operations of the fund, and this is reflected in their expense ratio.

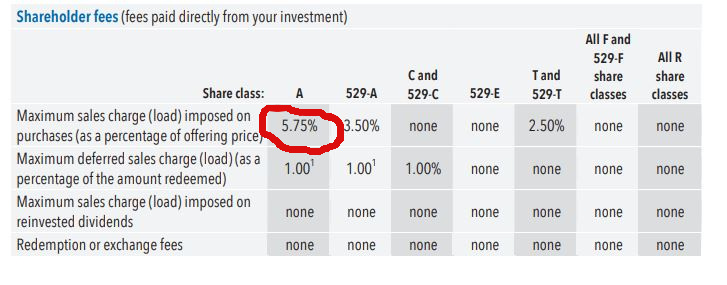

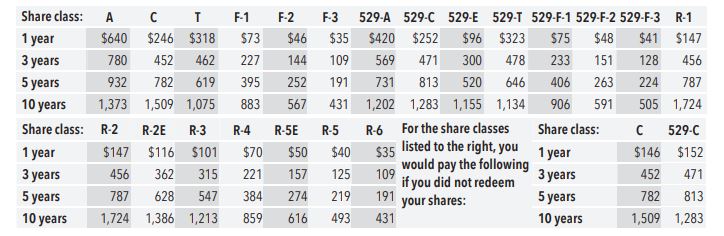

For an example, please refer to the prospectus for the AMCAP Fund. You should always refer to a fund’s prospectus before purchasing shares of it.

You can see, for example, the 5.75% maximum sales charge for class A share is clearly stated.

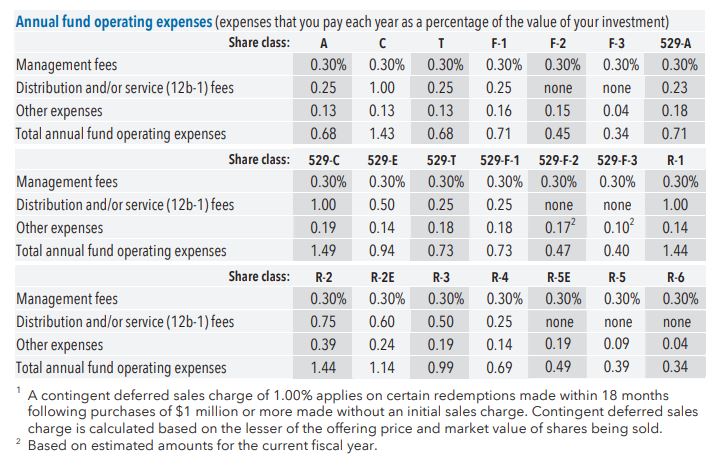

There is also a chart breaking out the fund operating expenses.

Importantly, the prospectus also illustrates what the cost of the fund would be over time given various assumptions.

How do you know if you are buying an A share mutual fund?

That’s all well and good, you may say, but how do I know if I own an A share mutual fund?

Even better: how do I know what share class of a fund I own, in general?

- First, you should know what share classes of the mutual fund are in fact offered, so that you can evaluate which share class meets your needs. Do your research before you buy it. This is all disclosed in the mutual fund’s prospectus. A copy is available online, or you can contact the company to have a copy mailed to you.

- Second, determine how you want to buy the fund. You can buy it directly from the mutual fund company or using your brokerage account. The fees may vary depending on how you go.

- When you enact a purchase transaction, you will be asked to specify which share class you want.

- After the trade is executed, you will receive a confirmation stating the ticker, amount, commission paid (if applicable), and share class. Remember to save this in your records in case you forget.

Another way for an investor to check is to go to the mutual fund website and check the Fact Sheet. It will list the various shares classes. Also, in many cases, you can tell by the ticker symbol. For example. PIMCO total return fund is PTTAX for the A share and PTTCX for the C share

Why A share mutual funds are not beneficial to investors

There are several circumstances that may lead an investment in A share mutual funds to benefit the issuing company and the person who sold it more than the investor. This is important for anyone thinking about buying an A share mutual fund to understand.

Here’s how an A share mutual fund will likely be sold to you, usually by a broker who wants to get a commission. Remember the sales load we discussed above?

- They’ll usually say that after you invest, you won’t pay any loads for the next 10 years, as you would with other share classes such as C shares who charge a redemption fee when you sell them.

- They also may make some claim that the 12b-1 fees are lower because of the sales load paid.

- They may even say that you can invest within the same fund family without having to pay another load.

We don’t see the logic of the argument for the following reasons:

- Even if you don’t, you’re still paying fees throughout the duration of the time you hold the mutual fund in the form of the fund’s internal operations, which tend to be higher than the expense ratios associated with holding other less expensive vehicles such as ETFs.

- High fees paid have a significant effect on the long-term performance of an investment. From the start, you have to earn the sales load back just to breakeven. Over time, the compound effect is a large detractor from wealth.

- If you want to avoid paying another load by going outside the fund family, you are inherently limited to whatever the options are within that fund family.

Make sure that any performance figures you use, whether in the prospectus, on the website, include the sales load. If not, you may be thinking the returns are higher than they really are. Usually, the company will publish a version of the figures with and without the load.

What to do before buying a mutual fund

Being an educated investor is of high importance. Before purchasing a mutual fund, do your homework.

#1

Read the prospectus. You can find it online or call the company to have a copy sent.

#2

Use online tools to determine the cost of what you are buying. Here are two mutual fund cost calculators:

Personal Fund mutual fund cost calculator

#3

Evaluate the full universe to determine if there are lower cost options available. This may take some time, but it is better to make a wise, informed decision. Websites such as Morningstar provide free research for the public

There are better options than A share mutual funds

In our view, we think A share mutual funds should be avoided by investors – and in fact, we are not a big fan of investing in mutual funds for our clients whatsoever. As a low fee financial advisor, we invest our clients’ money into low-cost ETFs and avoid high fees altogether. None of our clients’ money is invested into funds with loads, 12b-1 fees, or high expense ratios.

We are a fiduciary financial advisor in the Philadelphia area, but we work with clients across the country. We provide fee-only, objective advice to our clients on taxes, wealth management, and financial planning. If you would like to discuss a possible relationship, contact us.

Sources

Dalbar, Inc. 2020 QAIB Report for the period ending December 31, 2019. Retrieved from here.

Finra. Mutual Funds: Share Classes. Retrieved from here.

Investment Company Institute. 2021 Investment Company Face Book. Chapter 6: US Fund Expenses and Fees. Retrieved from here.

Mutualfunds.com. Decoding Mutual Fund Share Classes. Retrieved from here.

U.S. Securities and Exchange Commission. (12 May, 2014). Investor.gov. Investor Bulletin: Mutual Fund Fees and Expenses. Retrieved from here.

Capital Group. American Funds. Forms & Literature. Summary Prospectus, AMCAP Fund. Retrieved from here.